UK Visa Financial Requirements 2026: A Strategic Legal Guide for 2026

A single missing bank statement page is often the difference between a life in Britain and a mandatory refusal. The Home Office treats the uk visa financial requirements 2025 with clinical precision; they don’t offer leniency for administrative oversights. If your evidence fails to align with the specified rules, your application will likely be rejected. It’s a rigid system where technical compliance is just as vital as the income itself.

We understand that the shift to a £29,000 minimum income threshold has created significant anxiety for many families. This guide serves as your strategic map to ensure your evidence meets every strict standard. We’ll examine how to combine cash savings with employment income and clarify the transitional rules for those who applied before April 2024. You’ll gain total clarity on your category and learn how to build a package that withstands meticulous scrutiny. Proper preparation is your strongest defence against a costly refusal.

Key Takeaways

- Understand the rigid £29,000 minimum income threshold for new applicants and why the Home Office treats this as a non-discretionary legal barrier.

- Identify if you qualify for the lower £18,600 transitional threshold, ensuring you maintain a continuous visa route to avoid higher costs.

- Learn how to navigate the complex uk visa financial requirements 2025 by correctly categorising income from salaried employment, self-employment, or cash savings.

- Master the “Specified Evidence” rule and the 28-day rule to ensure your financial documentation is current and compliant at the precise moment of submission.

- Discover why a professional evidence audit is essential to mitigate the high emotional and financial costs of a visa refusal based on technicalities.

The £29,000 Minimum Income Requirement: Navigating the 2026 Landscape

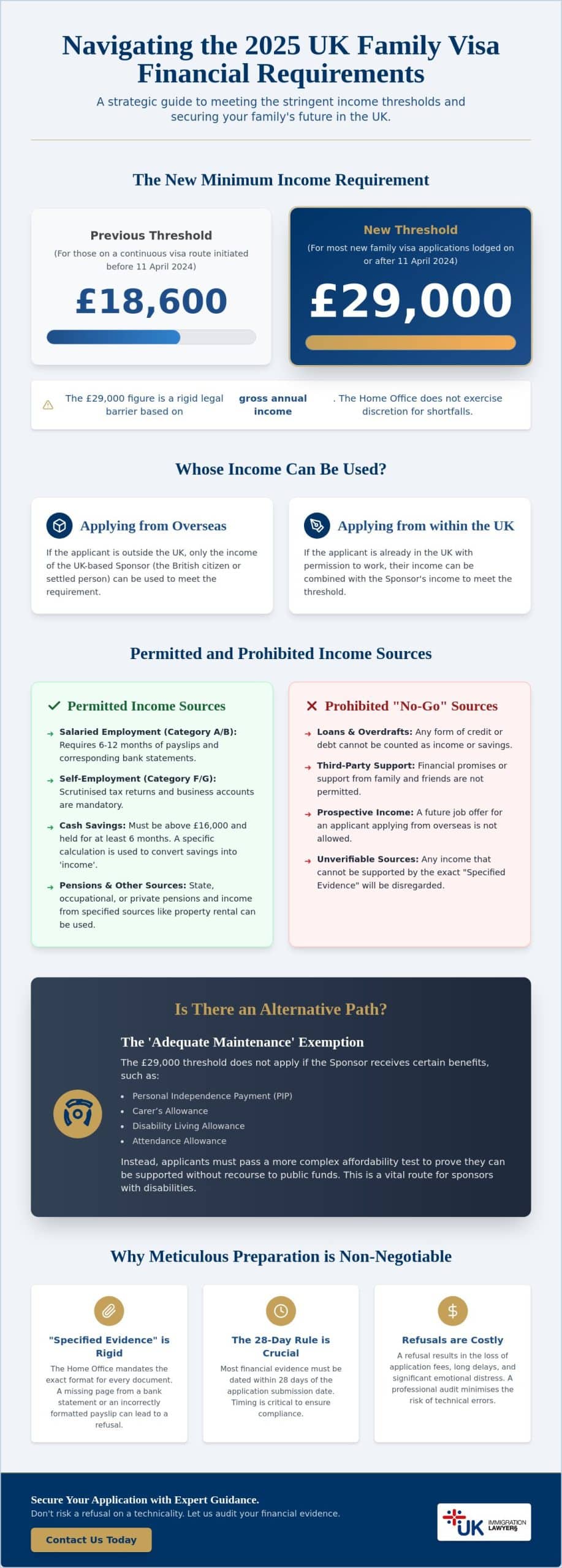

The landscape of British migration changed fundamentally on 11 April 2024. On this date, the Minimum Income Requirement (MIR) surged from £18,600 to £29,000 for most new family visa applicants. This shift was part of a broader overhaul of the UK’s points-based immigration system. When assessing the uk visa financial requirements 2025, you must understand that the £29,000 figure is a rigid legal barrier. The Home Office doesn’t exercise discretion if you fall short by even a small amount. Decisions are based on gross annual income, which is your salary before tax and National Insurance deductions. Your net take-home pay is generally irrelevant to this calculation.

Identifying who provides the funds is the first step in your strategy. The ‘Sponsor’ is the British citizen or settled person. The ‘Applicant’ is the person seeking the visa. If the applicant is applying from outside the UK, only the Sponsor’s income counts. If the applicant is already in the UK with a valid visa, their earnings can be combined with the Sponsor’s income. Meeting the uk visa financial requirements 2025 requires a precise understanding of these roles. Whilst there were previous discussions regarding further increases to £34,500, the threshold remains fixed at £29,000 for 2025 and 2026.

Who Must Meet the Financial Requirement?

This mandate applies to Spouse, Civil Partner, and Unmarried Partner visa applications. For those applying as a Fiance(e) or Proposed Civil Partner, the rules are often more restrictive. Since these applicants cannot work upon arrival, the Sponsor must usually prove they meet the full £29,000 requirement alone. A significant change in the 2024 rules involves dependent children. For new applicants, the threshold remains a flat £29,000 regardless of the number of children included. This simplifies the calculation but places a high burden on single-income households.

The Adequate Maintenance Alternative

A common oversight in visa planning is failing to check for the ‘Adequate Maintenance’ exemption. If the Sponsor receives specific benefits, such as Personal Independence Payment (PIP) or Carer’s Allowance, the £29,000 threshold doesn’t apply. You must instead pass a more complex affordability test. This test ensures the family can support themselves without relying on public funds. Adequate maintenance is a calculation of income minus housing costs. Whilst this alternative path is more complex, it’s often the only viable route for sponsors with disabilities.

Understanding Income Categories: From Salaried Employment to Cash Savings

Navigating the uk visa financial requirements 2025 necessitates a strategic choice between various income categories. The Home Office classifies income into distinct paths, each with its own evidentiary burden. Category A is the standard route for those who’ve been with the same employer for at least six months. If you’ve been with your employer for less than six months, you must apply under Category B. This requires proving you meet the official minimum income requirement over the last 12 months, which is a significantly more complex evidentiary task.

Categories F and G cover self-employment and limited company directorships. These categories are notoriously difficult because the Home Office scrutinises tax returns and company accounts with extreme rigour. If your business year doesn’t align perfectly with the application date, you risk a technical refusal. If you’re unsure which category applies to your specific employment structure, you may wish to speak with a specialist to review your payslips and accounts before submission.

Certain income sources are strictly prohibited by the Home Office. You cannot use loans, third-party financial support, or prospective income from the applicant if they’re applying from abroad. Relying on these “No-Go” zones is a guaranteed path to rejection. Every pound must be traceable to a permitted source and supported by the specific documents mandated by the Immigration Rules.

Salaried vs. Non-Salaried Income Logic

For salaried employees, the Home Office uses the “lowest monthly pay” received during the six-month period and multiplies it by 12. If your salary fluctuated, this calculation could leave you below the £29,000 threshold. Non-salaried income, such as hourly wages, is calculated by taking the average over the period. This distinction is critical. Choosing the wrong logic can result in an accidental failure to meet the uk visa financial requirements 2025 despite having sufficient total earnings.

The Cash Savings Formula for 2026

Category D allows you to use cash savings to bridge a shortfall or satisfy the mandate entirely. The formula is precise: (Savings – £16,000) / 2.5 = Income equivalent. To meet the £29,000 requirement using only savings, you must hold £88,500. These funds must be held in an “instant access” account for a minimum of six consecutive months. If the balance dips below the required amount for even a single day, the six-month clock resets. You must also prove the source of these funds to ensure they aren’t a temporary loan from a third party.

Transitional Arrangements: Rules for Extensions and Renewals in 2026

Applicants approaching a visa renewal in 2026 often face significant anxiety regarding the £29,000 threshold. However, the Home Office has established transitional arrangements for those who entered the family route before the rules changed. If you were granted leave as a partner or fiancé(e) before 11 April 2024, you remain eligible for the lower £18,600 threshold. This protection is not indefinite; it depends entirely on the “Continuous Route” principle. If you allow your visa to lapse or switch to a different, non-family category, you will lose this protected status. Maintaining your visa chain is the only way to avoid the higher uk visa financial requirements 2025 mandate.

Strategic planning is essential when your income has fluctuated between your initial grant and your 2026 renewal. If your earnings have dipped below the required level, you must identify this early. You might need to combine income with cash savings or wait until your average earnings over a longer period meet the threshold. The Home Office applies the rules with absolute rigour during extensions. They will not overlook a shortfall simply because you were successful in your initial application.

The £18,600 Legacy Threshold

The £18,600 requirement applies to individuals extending their stay with the same partner, provided they’ve held continuous leave on the route since before April 2024. These legacy rules are governed by the technical standards in the Immigration Rules Appendix Finance. Unlike the new flat-rate system, these transitional rules still require additional income for non-British dependent children. You must evidence an additional £3,800 for the first child and £2,400 for each subsequent child. Changing employers during this period is permissible, but it may force you from Category A into the more complex Category B calculation.

Switching Routes and the “New Rule” Trap

A common pitfall occurs when an applicant switches from a different visa category, such as a Skilled Worker or Student visa, into the family route in 2026. In these instances, you are considered a “new” entrant to the partner category. You must satisfy the full £29,000 uk visa financial requirements 2025 regardless of how long you’ve lived in the UK. There is no transitional protection for those moving between different visa tiers. Couples must evaluate their long-term residency goals carefully. If your ultimate aim is Indefinite Leave to Remain (ILR), ensure your financial strategy accounts for the higher threshold at every future renewal stage.

Evidentiary Standards: The Meticulous Expert Approach to Documentation

The Home Office rejects applications that are 99% correct. Under the “Specified Evidence” rule, your documentation must strictly adhere to the requirements set out in Appendix FM-SE. A common point of failure is the 28-day rule. This mandate requires your most recent financial document, such as a bank statement or payslip, to be dated no more than 28 days before the online submission. If your evidence falls outside this window, the caseworker will likely refuse the application without requesting further information. Precision is the only way to satisfy the uk visa financial requirements 2025.

To meet the uk visa financial requirements 2025, your employer letter must include five mandatory details. It must confirm your job title, your current gross annual salary, and how long you’ve been employed. It must also specify the period over which you’ve earned the salary relied upon and confirm the type of employment, such as permanent or fixed-term. Omitting even one of these details creates a technical vulnerability that caseworkers often exploit. Professional document organisation also influences caseworker behaviour. A well-indexed bundle, separated by clear dividers and accompanied by a schedule of documents, reduces the cognitive load on the official. If a caseworker can find information easily, they’re less likely to make an error or overlook a crucial piece of evidence.

Bank Statements and Payslips: A Mandatory Alignment

Every payslip must correspond exactly to a transaction on your bank statement. If the figures don’t match or if there are unexplained deposits, the Home Office may suspect third-party support or a temporary loan. Electronic statements are generally acceptable, but they must be properly authenticated or accompanied by a letter from the bank. Mismanaging these details is a primary cause of avoidable refusals. If you’re concerned about the quality of your documents, you should book a professional evidence audit to ensure your bundle is compliant.

The Role of the Legal Cover Letter

A “Letter of Representation” acts as a strategic guide for the caseworker. It maps your financial evidence to the specific categories of the uk visa financial requirements 2025. This is particularly vital for complex income structures involving bonuses, commission, or dividends. A professionally drafted legal cover letter pre-empts caseworker questions regarding income gaps by providing a clear, evidence-backed narrative. This document serves as a protective shield, ensuring the official understands the strength of your case before they begin their assessment.

Why Professional Representation is Vital for Financial Compliance

A visa refusal based on financial grounds is a preventable disaster. Beyond the emotional toll of family separation, the financial loss is absolute. The Home Office doesn’t refund application fees if you fail to meet the uk visa financial requirements 2025. A strategic legal approach ensures that every document is vetted against the current Immigration Rules before the submission button is pressed. It’s about building a case that’s impossible to ignore.

We conduct an exhaustive “Evidence Audit” for every client to ensure total compliance with the uk visa financial requirements 2025. This process involves cross-referencing every payslip with bank transactions and verifying employer details against Companies House records. If there are “Exceptional Circumstances” where a couple cannot meet the £29,000 threshold, we evaluate whether Article 8 of the European Convention on Human Rights (ECHR) applies. This legal argument can bypass financial mandates if a refusal leads to unjustifiably harsh consequences. However, the evidentiary threshold for such claims is exceptionally high.

Mitigating the Risk of Human Error

Human error in employer letters or bank statements accounts for a high percentage of technical refusals. Our review process identifies these invisible errors before they reach a caseworker’s desk. Having a regulated legal professional manage your case provides a layer of protection against the rigid and often unforgiving Home Office system. Ensure your financial evidence is flawless—book a consultation today.

Strategic Planning for ILR and Citizenship

Success today is only half the battle. You must manage your finances with an eye toward Indefinite Leave to Remain (ILR) and British Citizenship. Changes in your employment or business structure can impact your future eligibility for settlement. We help you organise your financial affairs to ensure a smooth transition through the 5-year route. Secure your future in the UK with expert legal guidance.

Securing Your Family’s Future in the United Kingdom

Meeting the uk visa financial requirements 2025 is a technical challenge that demands absolute precision. The Home Office prioritises rigid adherence to Appendix FM-SE over the underlying reality of your finances. Whether you’re navigating the £29,000 threshold for the first time or protecting your status under transitional arrangements, your evidence must be beyond reproach. A single missing document or a misaligned bank entry can derail years of planning and lead to an immediate refusal.

Professional management transforms a high-risk process into a structured legal strategy. We are regulated by the Immigration Advisers Authority and specialise in Appendix FM Spouse Visa applications. Our team brings deep expertise in managing complex financial category combinations and conducting meticulous evidence audits. If you want to ensure your application stands up to the highest level of scrutiny, Book a Specialist Immigration Consultation today. Your path to a life together in the UK is within reach when you approach the system with the right preparation.

Frequently Asked Questions

Can I combine my income with my partner’s income to meet the £29,000 requirement?

You can combine incomes only if the applicant is currently in the UK with a valid visa that permits employment. If the applicant is applying from overseas, the Home Office only considers the sponsor’s UK-based income. Combining incomes is a vital strategy for many couples already living in Britain who need to reach the higher threshold.

What happens if I lose my job just before I apply for my UK spouse visa extension?

Losing your job before an extension application is a critical issue because you must meet the uk visa financial requirements 2025 at the point of submission. If you’ve started a new role, you will likely need to apply under Category B. This requires proving your income over the last 12 months. Alternatively, you might rely on cash savings if they meet the £88,500 threshold.

Can I use my savings and my salary together to meet the UK visa financial requirements?

You can use cash savings to supplement a salary shortfall provided the savings exceed £16,000. Every £2.50 in savings above this baseline replaces £1 of annual income. For example, if your salary is £25,000, you would need £26,000 in savings to bridge the £4,000 gap to the £29,000 requirement. This combination is a common way to satisfy the mandate.

Is it possible to use rental income or dividends to meet the financial threshold?

Rental income and dividends are permitted sources of non-employment income under the Immigration Rules. You must provide specific evidence, such as a tenancy agreement for rental property or dividend vouchers for stocks. If you are a director of the company paying the dividends, different and more complex rules under Category F or G will apply to your application.

Does the Home Office accept income from overseas employment?

The Home Office typically ignores overseas employment income for the applicant. However, a sponsor returning to the UK can rely on their overseas earnings if they have a confirmed UK job offer starting within three months of their arrival. This specific exception allows families to relocate together without the sponsor having to move to the UK alone first.

What is the “28-day rule” for financial evidence in UK visa applications?

The 28-day rule requires that your most recent piece of financial evidence is dated within 28 days of your online application. This applies to your latest payslip, bank statement, or employer letter. If your documents are older than this at the moment you pay the application fee, the Home Office will likely refuse the visa on technical grounds.

Can I meet the financial requirement if I am self-employed but my business made a loss?

You cannot meet the requirement through self-employment if your business shows a loss. The Home Office calculates income based on the gross taxable profit as evidenced by your most recent tax return. If your profit is below the threshold, you must look to other permitted sources, such as cash savings, to satisfy the uk visa financial requirements 2025 mandate.

Are there any exceptions to the £29,000 minimum income requirement for 2025/2026?

Exceptions exist for sponsors receiving specific disability-related benefits or Carer’s Allowance, who must instead meet the “Adequate Maintenance” test. Additionally, those who applied for their partner visa before 11 April 2024 fall under transitional arrangements. These individuals only need to meet the legacy £18,600 threshold for their extensions, provided they maintain a continuous visa route.